In the 1985 movie “Lost in America” Albert Brooks plays David Howard, a yuppie advertising executive who saves $180,000, quits his job and buys a Winnebago to tour the country with his wife. When they visit Las Vegas, his wife loses all of their money playing roulette. In the funniest scene in the movie, a distraught Howard lectures his wife on the “Nest Egg Principle”. “The nest egg is sacred. We must never touch the nest egg. The egg is our protector and keeps us safe. Without the egg we have no protection.” At the conclusion of his lecture, Howard asks his wife to write “I lost the nest egg” one thousand times.

Baby Boomers should pay attention to Howard’s lecture about the Nest Egg Principle. In the coming years your nest egg may be in jeopardy.

Why?

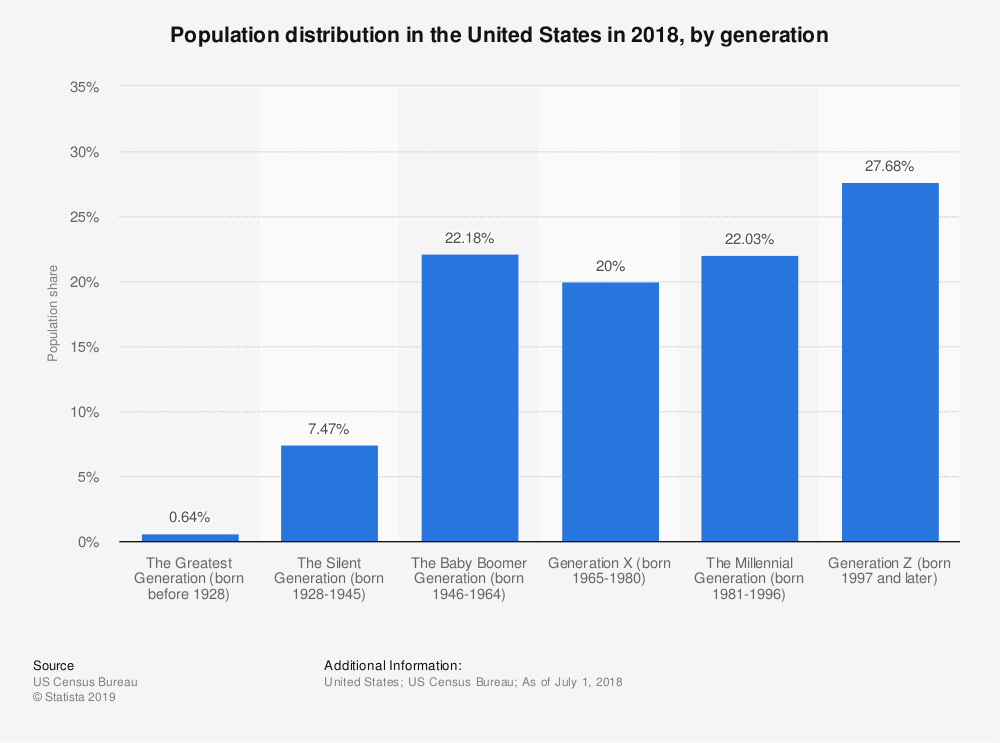

The explanation starts with demographics. The U.S. is divided politically by race, gender, sexual preference, immigration status and religion. Soon we will see another major political division emerge – a division by age. Baby Boomers, born from 1946 to 1964, have long been the largest age group, influencing social trends and controlling most elections, but that is about to change. Demographic data now show for the first time that Millennials outnumber Baby Boomers.

Millennials and GenZ

Millennials are those born from 1981 to 1996, so today they range in age from 24 to 39. Gen Z, the group that follows Millennials, includes those born from 1996 to 2020, so voting-age members of the Gen Z group are between 18 and 24.

Millennials and Gen Z together comprise 37% of eligible voters and this number will only grow as Boomers die off and more of Gen Z reaches age 18.

Shockingly to many Boomers, surveys show that unlike previous generations, Millennials and Gen Z have a favorable view of socialism. One poll shows that 70% would vote for a socialist. In another, more than half said they preferred “socialism” to “capitalism”[i].

Commentators have debated the reasons for this shift of opinion.[ii] One view has it that growing inequality in wealth and income is a leading cause. A shrinking middle class is another possible explanation. Similarly, underemployment due to offshoring and automation has also been a source of dissatisfaction. America has long been a place where each succeeding generation has surpassed the prior generation economically and this has set high expectations for Millennials. Unfortunately, those expectations are not being met by a significant percentage of the group. In fact, almost a quarter of Millennials still live with their parents. Many Millennials agree with Bernie Sanders that “the system is rigged.

Adding to the younger generation’s disillusionment with the economic system is their high indebtedness from education, auto loans and credit card balances. Current student loan debt is about $1.5 trillion, and because many graduates are underemployed, they are finding it difficult to repay their loans.

Not to say that the Millennials are monolithic. Some are obviously doing well economically, but a large percentage of the group do feel a sense of helplessness, like they’ve been cheated by the system. Many of them blame the older generation. Have you heard the popular pejorative – OK, Boomer? It’s meant to convey in a sarcastic way that Baby Boomers are not only clueless but responsible for the current bad situation in which many young people find themselves. The expression is especially popular with GenZ.

Perhaps amplifying this social dynamic is the fact that the Millennials and Gen Z are a much more racially/ethnically diverse group than Baby Boomers. About half of Gen Z is comprised of individuals who self-report to be in a minority racial category and many are from immigrant families.

What do Millennials and Gen Z want?

Since this block of voters will likely hold sway if not in the 2020 election, certainly in future elections, what will they demand of their elected representatives? That seems pretty clear. Let’s take a look at the platforms of the politicians who represent their interests — Bernie Sanders, Elizabeth Warren, and AOC, among others. Their platforms include proposals like:

- Expanded government health insurance,

- Free college tuition,

- Forgiveness of existing college loans,

- Universal guaranteed income,

- Government-funding of alternative energy sources.

These spending programs together will be very expensive, costing many trillions of dollars. The COVID-19 bailout has already cost a previously unthinkable sum, but the price tag for the Millennial/Gen Z programs will be many times larger. Even before the pandemic, in fiscal year 2019, the federal deficit was $1 T and the federal debt stood at about 120% of GDP. In fiscal year 2020, the deficit may reach $4T or more.

The developing scenario – very large deficits and demands by an increasing portion of the electorate to dramatically increase spending – leads to the inevitable conclusion that the federal government will need to find new and creative ways to increase tax revenue or somehow pull a rabbit from their hat.

Modern Monetary Theory – A Rabbit from the Hat?

A possible solution to this dilemma has been offered by economists following the school of thought called Modern Monetary Theory (MMT). According to this “have-your-cake-and-eat-it -too” theory, the size of the federal debt doesn’t really matter. One of the leading advocates of MMT, Prof. Stephanie Kelton of Stonybrook University, argues that unlike a business or a household which must repay its debts, the Federal Reserve can “print” large amounts of money to fund initiatives such as a guaranteed income program or public infrastructure projects. And, because the United States can borrow in its own currency, the logic goes, the increase in public sector debt poses no real danger to the economy[iii]. Any debt can be repaid by “digitally printing” more money and furthermore, because of the government’s ability to create money, debt is not even necessary.

Would MMT actually work? Most leading economists argue that implementing MMT would lead to a debasing of the currency and, as a result, inflation. Supporters of MMT sometimes point to Japan which has a debt/GDP ratio of 250% and has been employing a monetary policy that might be described as MMT Lite. Despite its high debt, the Japanese economy still grows, albeit very slowly over the past 30 years. Other economists say that what really counts is not the absolute debt but the net debt (debt minus public assets). According to Koichi Hamada, professor of economics at Yale University, “unlike the U.S., the Japanese government owns very valuable public corporations. So, by that measure (net debt/GDP) Japan and the U.S. are currently at parity”[iv].

A post-2020 government may use MMT logic to justify the higher deficits required to fund the Millennial wish list, but it will be only part of the solution. Deficit spending or money creation alone do not accomplish another one of the Millennial/GenZ objectives: to reduce inequality in income and wealth. Tax increases would be needed to accomplish this objective.

What taxes are most likely?

As Yogi Berra once said, “predictions are difficult, especially those about the future”. Instead of predicting, let’s review a list of the kinds of tax increases the government may impose.

Some politicians tell us that all future bills can be paid by increasing taxes on the top 1% of income earners, but that’s just not true. The top 1% earn an aggregate annual income of just over $2 trillion.[v] If the Government were to take an additional 20% of their income, that’s only $400 billion a year, a mere drop in the bucket compared to the size of the anticipated debt. What if the top 5% were the target? The combined income of the top 5% is approximately $5 trillion per year, so taking 20% of the total would yield $1.0 trillion in additional tax revenue. That would help, but it’s still not enough. Also, there’s the issue of whether such a tax program could actually be successful. Would people like Bill Gates, Jeff Bezos and Mike Bloomberg stand by and watch the government take 20% more of their income? I doubt it. As very large political contributors, they can seek favors from politicians and, because of their vast resources, they can hide their income in countless ways.

New spending programs cannot be fully funded with personal income taxes because the debt is large compared to the amount of income that could be taxed, the ultra-wealthy would find ways to avoid taxes and imposing very high tax rates may actually cause tax receipts to decline. Other tax programs would be needed in addition to raising personal income tax rates.

Taxes on Business

Business income taxes include taxes on corporations (C corporations) as well as pass-through entities (S corporations, LLCs, partnerships and sole proprietorships). Income from the latter group passes through to the owners who must include it as part of their personal income for tax purposes. The ‘Tax Cuts and Jobs Act of 2017’ (TCJA) allows pass through entities to deduct 20% of qualified business income. The TCJA also cut the statutory corporate tax rate from 35% to 21%. This reduced corporate tax receipts by almost $100 billion in 2018 as compared to 2017. In recent years corporate income taxes have totaled only 15-20% of personal income taxes.

Candidate Joe Biden has proposed reversing the TCJA, eliminating the 20% deduction for pass-through entities and increasing the corporate statutory rate back to 35%. This would probably increase tax revenue by $100 to $200 billion, assuming it did not trigger layoffs which it very well may. This tax would also help to reduce income inequality because many in the top income categories receive much of their income from private businesses.

Unrealized Capital Gains

Elizabeth Warren proposed during her 2020 Presidential Campaign, a “mark-to-market” tax on unrealized capital gains, i.e., appreciation in stock portfolios, real estate or other assets. With the run-up in stock market and real estate values over the past 10 years, taxing unrealized gains would certainly give the Government access to a huge new tax stream, but fully implementing this kind of a tax would be difficult. It would require that the cost basis and fair market value of all assets be estimated and verified. This may be fairly straightforward for financial assets but would be more difficult for other kinds of assets. Even if the tax were limited to financial assets, taxing unrealized gains would not only generate tax revenue but would also serve to reduce the wealth of more affluent households. However, a problem with such a tax from the government’s perspective is that the revenue yield would be very unpredictable from year-to-year. In the first year the tax is implemented it would produce a huge windfall, but in subsequent years tax receipts would rise and fall with the stock market. For that reason, a tax on unrealized capital gains may not be the government’s first choice for raising additional revenue.

Estate Tax

According to the IRS, “The Estate Tax is a tax on your right to transfer property at your death. It consists of an accounting of everything you own or have certain interests in at the date of death. The fair market value of these items is used, not necessarily what you paid for them or what their values were when you acquired them. “

Currently estates are taxed 40% by the federal government for amounts in excess of $10.58 million. Sen. Bernie Sanders has proposed raising this rate to 77% and reducing the dollar threshold. This is a hot button topic for Sanders and others who believe wealth should not be passed from one generation to the next. Expect to see this kind of change in the tax code.

Wealth Tax

Another proposal Sen. Warren put forth is to tax wealth.

What’s included in “wealth”? Wealth is an individual’s or couple’s net worth, their assets minus their liabilities. Assets include savings, brokerage accounts, retirement accounts, real estate, vehicles, art, precious metals, and private businesses. Liabilities include mortgages, home equity loans, business loans, and any other debt

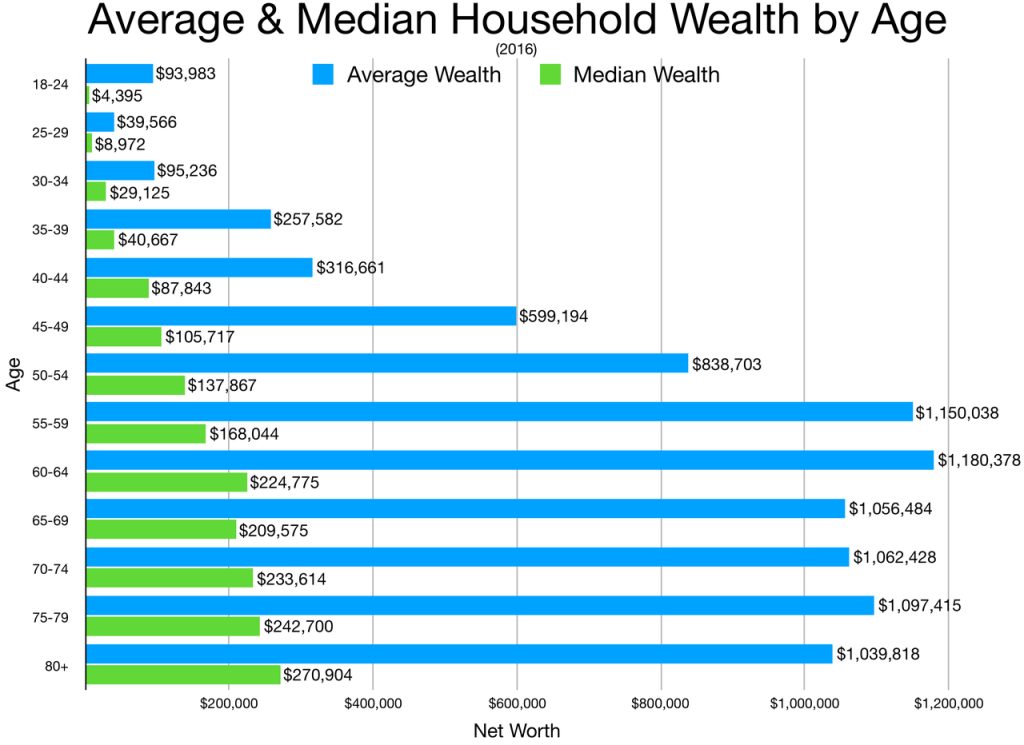

The distribution of wealth, like income, is very skewed toward a small group of the most affluent. The richest 10% of households own 70% of the wealth.[vi] And, a very large portion of aggregate wealth is held by Baby Boomers, those over 55 years old who have accumulated savings over many years.

Herein lies the future battle between Baby Boomers who have accumulated wealth and Millennials/ GenZ who feel cheated and entitled to more. The most direct way for politicians to redistribute wealth is to tax it. And, this is the biggest threat to Baby Boomer Nest Eggs. The Boomers have the money and the Millennials want it.

Current household wealth in the U.S. is about $100 trillion[vii]. Sen. Warren suggested taxing wealth at 2% per year for wealth above $50 million and an additional 1% for wealth above $1 billion during her 2020 bid for the Democrat nomination. Billionaires, Michael Bloomberg and Howard Schultz, criticized the proposal as unconstitutional, but many legal scholars disagree. Independent economists estimated that Sen. Warren’s proposal would generate about $275 billion in tax revenue each year. That’s obviously not enough. To make a big difference in the federal budget the wealth tax would need to be broadened to include households with less than $50 million in assets. In the worst (or best) case, if the tax were applied to all household wealth, that would generate $2 trillion in tax revenue per year, enough to fund many of the Millennial/GenZ programs.

Household wealth could be the pot of gold that politicians need to get elected with Millennial/GenZ votes in the future. After all, Boomers are dying off; they’re not going to be determining election outcomes in the future. It’s Millennials and GenZ who will hold sway in elections from now on.

Source: www.dqydj.com

Has a Wealth Tax Ever Been Tried?

Fifteen other countries have tried wealth taxes and four countries (Switzerland, Norway, Spain, and Belgium) still have wealth tax programs in place.

In France the wealth tax was repealed because too many wealthy taxpayers fled the country, reducing the tax base. In 2017 it was replaced with a national property tax. [viii]

In Switzerland, Norway and Spain the wealth tax covers real estate and financial assets. The taxes affect not just the wealthiest, but also households of more modest means. For example, in Switzerland the tax is graduated and affects the top 34%. Anyone with a net worth above the equivalent of US$102,000 is taxed. In Norway the tax affects anyone with assets above the equivalent of US$181,000. .[ix] And, in Spain, the tax is levied on net worth in excess of US$774,000. The wealth tax in Belgium is imposed only on financial accounts above US$550,000.

In Switzerland net worth is self-reported and enforcement is lax. Academic studies show that wealth tax avoidance in countries where it has been tried is common. One study found that for each 1% increase in the wealth tax, the amount of reported wealth declined by 34%.

Besides taxpayer flight and tax avoidance, another challenge in implementing a wealth tax is valuation of assets. Valuing financial assets is straightforward and valuing real estate, although there is more leeway, is not difficult. But, valuing private businesses is not straightforward and it has been a source of conflict between taxpayers and European governments that have imposed wealth taxes. This is a non-trivial problem since it’s reported that the 1% wealthiest households in the U.S. have 40% of their wealth in private businesses. [x]

Support for Wealth Taxes in Academia

In 2014, French economist Thomas Piketty published a widely-discussed but controversial book entitled Capital in the Twenty-First Century. He starts with the observation that economic inequality is worsening and proposes wealth taxes as a solution. The central thesis of the book is that inequality is not an accident, but rather a feature of capitalism, and can only be reversed through state intervention.

Emmanuel Saez and Gabriel Zucman, two Economics professors from Berkeley, worked on the “Ultra-Millionaire Tax” proposed by Senator Elizabeth Warren. In their paper, “Progressive Wealth Taxation,” they present arguments for a wealth tax as a way to redistribute wealth.[xi]

Of course, these ideas have been taught in every university in the country, so it’s probably not surprising that recent grads may hold the same beliefs. As the surveys show, a high percentage of younger generations favor socialism or social programs like those put forth by the 2020 Dem candidates. And, they believe that wealth is unfairly distributed in the U.S. and indeed around the world.

So, a tax on wealth could very well gain support of the majority of voters. Millennials and GenZ will demand bigger social programs and wealth redistribution and politicians will need to deliver the goods to get re-elected.

What Can Baby Boomers Do?

Baby Boomers are in a vulnerable position. They’ve accumulated assets over a lifetime of work. They’ve already paid income taxes on at least part of their assets. If they were to lose their entire nest eggs in Las Vegas playing roulette or part of their nest eggs to a wealth tax, they would have little chance of recovering.

A wealth tax could be passed as soon as 2021, but because of the need for administrative changes and new IRS auditors to manage such a program, the Government may need to wait until tax year 2022 to make it effective.

What can Boomers do? Obviously, if you don’t want to be a sitting duck target for a wealth tax, start moving or redistributing assets. Of course, without knowing the provisions of the tax, that is easier said than done. Will the tax be levied on all assets, just financial accounts (like the tax in Belgium) or financial accounts and real estate (like Switzerland, Norway and Spain)? Will the IRS turn a blind eye to accounts held overseas (as Switzerland does and France apparently did)? No one knows. The politicians will consider factors like revenue generation, ease of implementation, backlash from political contributors, and flight of the wealthy. Without knowing the details of the tax, we cannot know exactly what we should do now, but again, let’s review the possibilities.

In the past, the wealthy commonly parked funds in overseas accounts in Switzerland, the Cayman Islands or other tax havens. Indeed, a Financial Secrecy Index produced by the Tax Justice Network ranks Switzerland and the Cayman Islands as two of the top places for hiding private wealth. The same report estimates that $21 trillion to $32 trillion worth of private wealth is located in what it calls “secrecy jurisdictions” around the world where the money is lightly or entirely untaxed.[xii] The old tax dodge was to minimize income taxes. That still exists, but the U.S. government is going to great lengths to clamp down on tax havens and this will affect taxpayers’ options for avoiding a wealth tax.

In 2010 Congress passed the Foreign Account Tax Compliance Act (FATCA) which requires all non-U.S. foreign financial institutions (FFIs) to search their records for customers with a connection to the U.S., including indications in records of birth or prior residency in the U.S., or the like, and to report the assets and identities of such persons to the U.S. Department of the Treasury.[xiii] FATCA also requires such persons to report their non-U.S. financial assets annually to the Internal Revenue Service (IRS). As a result of FATCA, the U.S. has signed compliance agreements not only with the Swiss government, but also with the governments of other once-favored tax havens like the Cayman Islands, Bermuda and Mauritius. Currently, Monaco and many African and Asian nations have not agreed to comply with FATCA.[xiv]

In addition to FATCA, under Bank Secrecy Act regulations issued by the Financial Crimes Enforcement Network, U.S. tax filers are required to report on foreign financial accounts exceeding US$10,000 on their tax returns.[xv] Therefore, to comply with current regulations, if cash or other assets were moved offshore, the assets would need to be moved outside of the international banking system.

What about overseas real estate? As of the 2019 tax year, the IRS does not require individuals to report international real estate holdings. Property taxes on international real estate can be itemized as a deduction and rental income must be reported, but the holdings and value of the holdings need not be reported. If the real estate is owned by a corporation and not the individual, then the foreign corporation must be disclosed on the individual’s tax return.

In February 2014, the Organization for Economic Development (OECD), also known as the G20, first presented a new global standard for information exchange, the Common Reporting Standard (CRS), a broad system of automatic information exchange between nations. The CRS does not include any provision for exchanging information regarding real estate holdings. It’s possible that owning international real estate in the right country may be a way to free assets from taxation.

A few years ago, some financial advisors were touting cryptocurrencies as a way to place funds out of reach from the government, but the IRS, (presumably fearing that crypto is a way for drug cartels to launder money or for terrorist organizations to secretly exchange funds), is clamping down on that strategy. They have recently asked Coinbase for a list of all of their account holders and for buy and sell data.[xvi] Also, 2019 is the first tax year in which filers must report on their crypto investment gains, but buying cryptocurrencies from an international exchange may still be a good way to secure assets and stay within the law. The CRS does not cover cryptocurrencies.

Another strategy would be to liquidate brokerage accounts, IRAs, and real estate investments and store cash in a home safe or other secure location. One could also invest in precious metals, art work or collectables. To comply with the Patriot Act, financial institutions must report any account withdrawals above $10,000 to the IRS[xvii], so withdrawing the money in small increments may be a good idea.

Baby Boomers could transfer assets to children to reduce net worth, but transfers above $15,000 are subject to gift tax. Also, the IRS sets an $11.4 million tax-free lifetime limit on gifts.

One could also take a low-interest loan to reduce net worth and shield assets from taxation. With interest rates so low, that may not be a crazy idea.

Historically, the very wealthy have sheltered income by setting up shell companies overseas or sometimes networks of interlocking foreign corporations, making it very difficult for the IRS to untangle the web to find funds. With the help of the best accountants and tax attorneys, the wealthiest will find ways to avoid a wealth tax using similar schemes. For all but the top .1% these kinds of strategies are currently not as attractive because of the cost, but clever, entrepreneurial law and accounting firms may start offering these services as a wealth-tax shelter to those in the 90 to 95 percentile categories.

The bottom line is if a wealth tax becomes law, it will be too late to secure assets. We obviously don’t yet know the tax rates that will be imposed, the wealth levels that will be affected, the loopholes that will be left open, or how vigilant the IRS will be in enforcing the law. To avoid taxpayers fleeing the country, like what happened in France, the IRS may take more of a lax-enforcement approach, as Switzerland does.

However, in a worst-case scenario, many retirees may be faced with an awful choice– to pay the wealth tax and sacrifice much of their nest egg savings or renounce their U.S. citizenship and move to another country. Renouncing U.S. citizenship would mean Baby Boomers would need to forego all future social security and Medicare benefits (and possibly even private pension benefits), after having paid into these programs for many years, but that may still be cheaper than sacrificing 2% of net worth every year. Those owning private businesses would obviously need to sell their businesses before the tax becomes effective.

Foreseeing the possibility of taxpayer flight, Sen. Warren’s plan would place a 40 percent exit tax on any U.S. taxpayer who renounces their citizenship and flees the country. This tells us that the politicians are willing to play hardball with Baby Boomers to achieve their objectives. To avoid such an exit tax, one would need to leave the country and move all assets before such a tax would take effect.[xviii]

The Nest Egg Principle Revisited

A strong case can be made that a wealth tax will be imposed and, because of the need to raise huge sums, will affect not just the ultra-wealthy but also perhaps those in the top 10%. Taxing the top 10% (those with a net worth of $1.2 million, based on 2017 wealth data) would give the IRS access to 70% of household wealth.[xix].

A wealth tax would hurt billionaires and other ultra-high net worth individuals less, not only because of their much bigger financial cushions but also, as mentioned, because they would be able to find many more ways to avoid taxes by: finding loopholes in the law and cleverly engineering their finances. Billionaires may also lose less by leaving the U.S. and moving to another country. As mentioned, for the ultra-wealthy, losing Medicare and Social Security benefits would be trivial in comparison to losing 2% of their wealth each year.

This is a good time for individuals who are 55+ to remember the Nest Egg Principle. For retirees, “the nest egg is sacred.” Many Baby Boomers need their nest eggs to maintain their standards of living during retirement and some, to pay for necessary expenses. Boomers should start making plans now to protect their nest eggs in case a wealth tax is imposed. After the tax becomes law, it will be too late.

About the author: David Stahl is a baby boomer and vigilant nest-egg watcher. He is retired from 25 years of investing venture capital in technology start-up companies and currently teaches MBA classes part-time. He has been to Las Vegas a number of times to attend trade shows, but has never played roulette.

[i] https://www.salon.com/2019/10/29/new-poll-finds-70-of-millennials-say-theyre-likely-to-vote-for-a-socialist/

[ii] https://www.businessinsider.com/millennials-would-vote-socialist-bernie-sanders-elizabeth-warren-debt-2019-10

[iii] https://www.weforum.org/agenda/2019/07/japans-answer-to-economic-deficit/

[v] https://taxfoundation.org/summary-latest-federal-income-tax-data-2018-update/#:~:text=In%202016%2C%20the%20top%201,percent%20of%20all%20income%20taxes.

[vi] https://www.marketwatch.com/story/the-richest-10-of-households-now-represent-70-of-all-us-wealth-2019-05-24

[vii] https://www.brookings.edu/blog/up-front/2019/06/25/six-facts-about-wealth-in-the-united-states/#:~:text=1.,total%20assets%20minus%20total%20liabilities.

[viii] https://en.wikipedia.org/wiki/Wealth_tax#cite_note-49

[ix] https://en.wikipedia.org/wiki/Wealth_tax

[x] The Problem with a Wealth tax, Wall Street Journal January 11, 2012

[xi] https://en.wikipedia.org/wiki/wealth_tax

[xii] https://fsi.taxjustice.net/en/methodology/secrecy-indicators

[xiii] “Sec ii B 1 Agreement between the government of the United States of American and the government of the United Kingdom of Great Britain and Northern Ireland to improve international tax compliance and to implement FATCA” (PDF).

[xiv] https://www.ustaxhelp.com/which-nations-have-igas-with-the-united-states/

[xv] https://en.wikipedia.org/wiki/Bank_Secrecy_Act

[xvi] https://www.coinbase.com/bitcoin-taxes#paytaxes

[xvii] https://www.reedsmith.com/en/perspectives/2001/12/banking-aspects-of-the-usa-patriot-act#:~:text=5311%20et%20seq.%2C%20and%20related,reported%20on%20suspicious%20activity%20reports.

[xviii] https://www.accountingtoday.com/articles/democrats-love-a-wealth-tax-but-europeans-are-ditching-the-idea

[xix] https://equitablegrowth.org/the-distribution-of-wealth-in-the-united-states-and-implications-for-a-net-worth-tax/