Imagine, if you will, a utopian land in which the needs of all residents are provided by the ruling authority. Consider further that the government of this land has at its disposal an unlimited supply of funds to serve its residents even without imposing taxes.

Imagine, if you will, a utopian land in which the needs of all residents are provided by the ruling authority. Consider further that the government of this land has at its disposal an unlimited supply of funds to serve its residents even without imposing taxes.

No, this isn’t an old episode of the Twilight Zone or a plot from a science fiction movie. It’s actually a scenario envisioned by a group of progressive economists. The theory underlying the vision is called Modern Monetary Theory (MMT), it’s gaining in popularity, and its leading proponent, Stephanie Kelton of Stonybrook University, has become somewhat of a celebrity. So, what’s MMT all about? To understand MMT, we need to review some basics about how the federal government operates today.

The Federal Budget

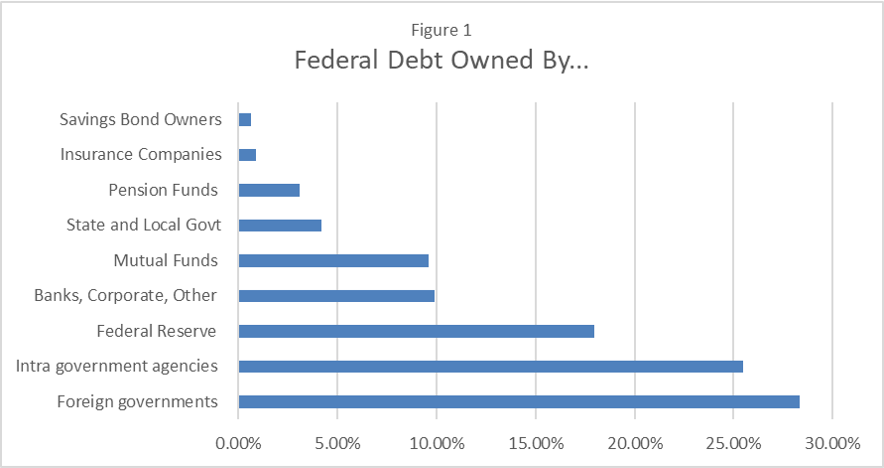

As most people are reminded every April 15th, the primary source of government funding is the tax revenue it collects from households and businesses. The government uses this money to fund its expenses including the military, the Washington bureaucracy, social welfare programs, safety net programs, and the interest on the debt. When spending exceeds revenue, like it did in 2019 by a whopping trillion dollars, the government sells bonds to cover the difference. As Figure 1 shows, bonds are purchased by foreign governments, other federal agencies, the Federal Reserve, commercial banks, corporations, mutual funds, and others.1 About 43% of federal debt is currently owned either by the Federal Reserve or other federal agencies. Bonds sold by the U.S. Treasury are backed by the integrity and creditworthiness of the federal government and are generally considered zero risk or at least very close to it. Because of their low risk, interest on Treasury bonds is low compared to the interest paid on almost all corporate bonds.

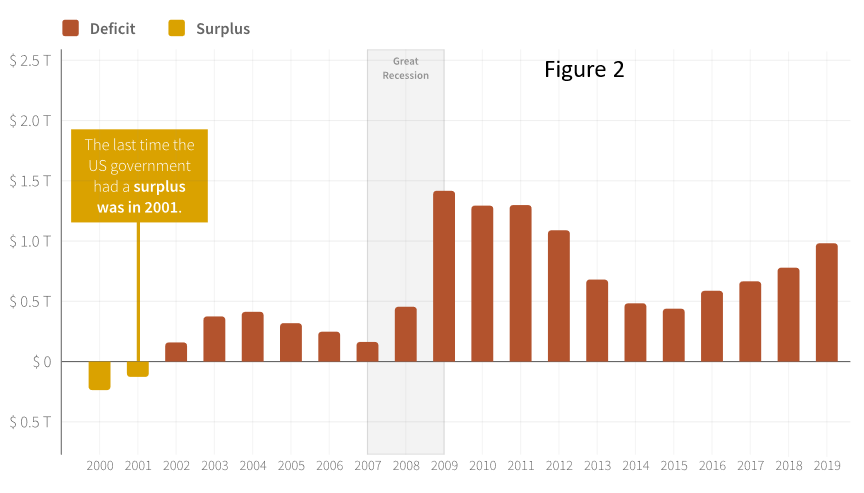

How is the government doing in terms of managing its debt? Not so good. As shown in Figure 2, the government has been running budget deficits since 2001. During the years following the 2008 credit crisis, the deficit increased to over $1 trillion for four consecutive years. In 2019 the deficit fell just short of $1 trillion and in 2020, with the huge COVID-related expenditures, the deficit is expected to exceed a previously unthinkable amount – $4 trillion or more.

As the debt has increased, so have interest payments on the debt. The Brookings Institute reports “Even at current low rates, the government spent about $260 billion on interest in the first eight months of the fiscal year 2020, roughly equal to the combined spending of the Departments of Commerce, Education, Energy, Homeland Security, Housing and Urban Development, Interior, Justice, and State. And, of course, if interest rates rise, the government’s interest tab will go up.”2

Often when the subject of fiscal debt is discussed, John Maynard Keynes is remembered. He was a famous early 20th century British economist whose ideas fundamentally changed the field of macroeconomics. Among his many new ideas, Keynes taught that governments use deficit spending to stimulate economies during lean periods but then run budget surpluses during high-growth periods. Following Keynesian doctrine, the U.S. ran large deficits during WW2 but after the war had many years of budget surpluses to repay the debt. However, since the 1970’s the U.S. has experienced only one period of budget surpluses and that was during the Internet boom period of the late 1990’s – early 2000’s. Since then the second part of Keynes’ message (i.e., that economies run surpluses during high-growth periods) has largely been forgotten by most government politicians. Germany is about the only capitalist country in the world that still runs budget surpluses during strong economic times. In all other nations around the world politicians have become addicted to deficit spending across the entire business cycle. Keynes would not approve.

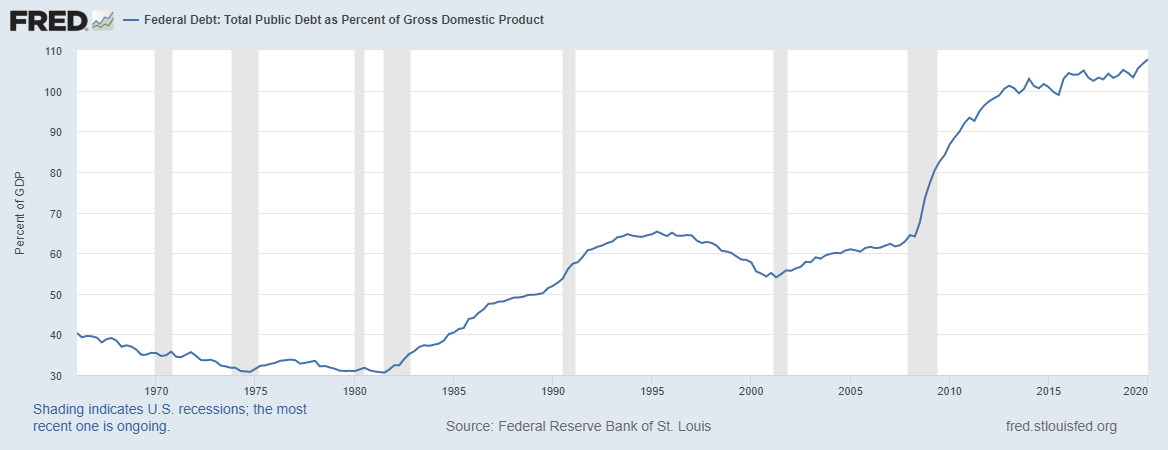

Should we be concerned about the growing debt? A partial answer to this question is provided by looking at the ratio of cumulative federal debt to GDP. This ratio is meaningful because a larger debt to GDP ratio translates to more difficulty repaying the debt. If the ratio becomes too high, even paying the interest on the debt may become problematic. Nobel laureate, Paul Krugman has often argued that if the GDP is growing as fast or faster than the debt, then debt poses no problem. In other words, Krugman is saying that the debt never has to be repaid, it can be rolled over when it comes due and the interest can be paid out of a growing budget each year. This is not a unique idea but a relatively new way of thinking about debt i.e., that it need never be repaid. However, unfortunately, as Figure 3 shows, the economy has not lived up to Krugman’s more permissive criteria for the past ten years. Over the past ten years the total debt has grown much faster than GDP. As of 2020, the ratio of debt to GDP is higher than it was at the end of WW2. Remember that WW2 was followed by a long period of fast economic growth and hence budget surpluses. There’s not much evidence to suggest that we are about to repeat that today. In this respect, the U.S. is in a unique situation in its history and not in a good way.

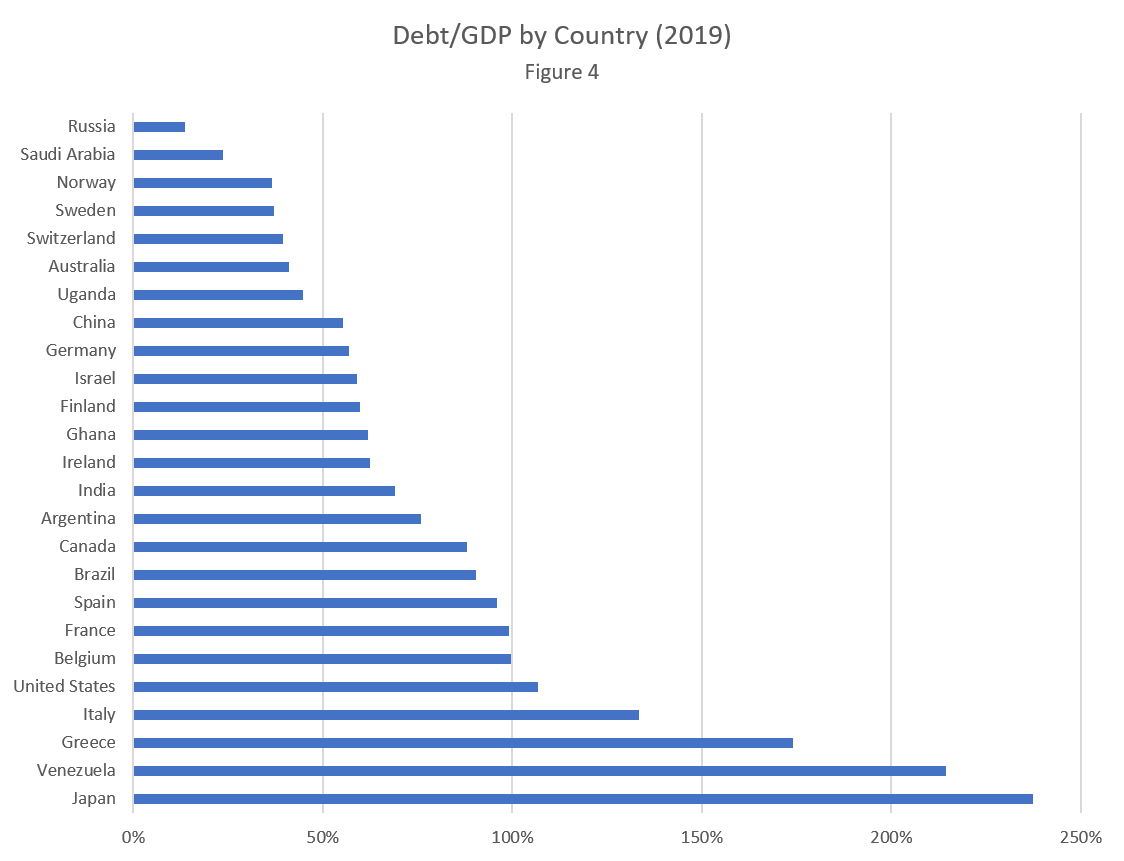

To see the current situation the U.S. faces relative to other countries, see Figure 4 which shows the Debt-to-GDP ratio by country for a select list of countries as of 2019.3 You can see that the U.S. is one of the most indebted countries on the list, exceeded only by Italy, Greece and Venezuela, (no surprises there) and Japan (I’ll be discussing Japan later). Notice that U.S. debt/GDP far exceeds that of Brazil and Argentina, two countries that have experienced debt crises and hyperinflation in the past.

So, how do we assess the situation the U.S. faces? I think anyone would have to agree that the current and rising debt poses a risk to the U.S. economy, currency and dominant position in the world.

This raises a most obvious question: Can the U.S. dig itself out of this debt hole? Studies show that countries with Debt/GDP ratios exceeding 130% do one of several things: restructure the debt (i.e., pay creditors a portion of what’s owed), devalue the currency to pay the debt in cheaper money, create lots of new money triggering high inflation, or outright default. What will the U.S. likely do? To answer this question, we need to discuss the Federal Reserve Bank of the U.S. which will play a key role in any strategy to address this problem.

The Federal Reserve Bank

The Federal Reserve Act of 1913 established the Federal Reserve Bank of the U.S. As provided for in the Act, the Board of Governors of the Fed are appointed by the President and confirmed by the Senate. Although the Chairman of the Fed is often asked to testify before Congress, the Fed operates independently and is not directly subordinate to the Executive or Legislative Branches. Of course, Congress could vote to abolish the Fed by overturning the Federal Reserve Act, but that’s rarely been discussed by anyone other than a few members of Congress, most notably former Congressman Ron Paul.

Some readers may be surprised to know the great influence the appointed (unelected) Fed Governors have over the economy. The Fed manages monetary policy with the dual objective of limiting consumer price inflation to a target of 2% and promoting job creation to achieve a target unemployment rate of 4-5%. They do this:

1. by setting the discount rate (the interest rate the Fed charges commercial banks for short-term loans),

2. by setting banks’ reserve requirements (the portion of deposits that banks must hold in cash, either in their vaults or on deposit at a Reserve Bank),

3. via open market operations (the buying and selling of government securities), and

4. by setting the interest rate paid by the Fed on excess reserves held for banks.4

The Fed can also fine tune an expansionary policy by implementing offsetting measures. For example, when the Fed makes bond purchases under open market operations, adding to the money supply, they can “sterilize” the purchases by taking money out of the economy at the same time. They may do this by having banks hold more reserves by requirement or enticement. They can also adjust bond maturities.

One of the most interesting aspects of Fed operations is their power to create money. In times past, new money was created by printing new paper bills. Today, in the day of digital transactions, the Fed produces new money simply by drafting an account on its books. In fact, the Fed can create as much money as it sees fit or, that is to say there are no legal restrictions on the amount of money it can create. The money the Fed creates is used for its “open market operations”, i.e., to purchase Treasury bonds or other securities.

Quantitative Easing During the Credit Crisis

During the 2007-2008 credit collapse, when the economy appeared to be on the precipice, the Fed implemented what Chairman Ben Bernanke called “credit easing” or what the press loosely referred to as quantitative easing (QE). The QE program consisted of three parts:

• Lending to financial institutions

• Providing liquidity to key credit markets (via loans and asset purchases)

• Purchasing longer-term securities (or, as they called it, “large-scale asset purchases”, LSAPs)

Although all parts of the program were important, we will discuss here large-scale asset purchases (LSAP), which received the most attention in the press and is most germane to this discussion. This program consisted of the Fed purchasing government bonds and other long-term securities with newly created money.5 The money was created with a snap of the fingers, a wave of a magic wand or actually a vote of a Fed committee. The Fed creates money and then records the bonds as an asset on their balance sheet. Astute accountants will at this point be saying to themselves “hold on just a second, what’s the offsetting entry on the balance sheet?” Well, indeed there is an offsetting liability. The amount spent on government bonds (the money creation part of the transaction) is recorded as commercial bank reserves, an amount owed to the commercial bank that sold the bonds.6 With more reserves, the bank is then able to loan more money to its customers. The net effect is the creation of money to increase the reserves of banks so they can loan more money to their customers. The transaction increases the supply of money and stimulates economic activity.

The original idea was to use QE as a stop-gap measure to help the economy recover from the credit crisis. The Fed’s plan was to unwind QE as the economy improved by selling the securities it had purchased. However, as fate would have it, the economic recovery was slower than expected, so the Fed continued the program for many years. QE, money creation by the Fed and near-zero interest rates became institutionalized.

The massive inflow of money into the financial sector from QE was supposed to spur business financing and consequently, business investment and new job creation. But, with weak consumer demand, businesses were reluctant to take on debt. What QE did instead was contribute to a huge boom in the stock market and markets for other financial assets. QE has also helped to keep Treasury rates low, which has helped the federal budget. Consumer prices have not been affected much because very little QE money trickled into the consumer economy.

Quantitative Easing During COVID

To counter the devastating economic effect of COVID, the Fed has expanded QE. Remember all of the hand wringing over the government bailout in 2008? The 2020 QE program makes 2008 look insignificant by comparison. At the end of 2007 the Fed owned about $745 billion in government securities7 but as of mid-August 2020, that number had increased to $4.3 trillion.8 That’s an increase of about 500% in 13 years. Fed bond purchases have helped the Treasury grow its debt to what is estimated to be 140% of GDP by the end of 2020 while maintaining very low interest rates on government bonds.

Japan and Abenomics

The current situation in the U.S. (high debt and slow growth) resembles the situation that Japan has faced for many years. Referring back to Figure 4, we see that Japan is the most indebted country in the world in terms of Debt/GDP. Yet, Japan has not suffered any devastating economic consequences. Why is that? In 2012 newly-elected Prime Minister Shinzo Abe championed a new economic policy to boost Japan’s economy. Abe recognized that because of Japan’s aging and shrinking population, the after effects of the 2008 credit crisis and moribund economic growth, extraordinary measures were needed to stimulate growth. Like the U.S., Japan has turned to quantitative easing and deficit spending to stimulate its economy. “In 2014, the Bank of Japan (BOJ) started a large-scale asset purchase program that purchased assets worth $660 billion dollars annually. The goal was to continue the asset purchases until the country’s inflation rate hit the target rate of 2%. In 2016, the BOJ lowered interest rates past zero to increase lending and investment. As of 2018, the short-term interest target was at -0.1%.” However, unlike the U.S., since 2014 70% of all Japanese government bonds have been purchased by the central Bank of Japan and the remainder by Japanese banks and trust funds.9 Huge deficits from stimulus programs over the past 20 years have caused Japan to run-up their debt to 250% of GDP. Like the U.S., money creation in Japan has not caused inflation in consumer prices.

So, to some, the experience of Japan is empirical evidence that debt really doesn’t matter, however not everyone is convinced that Japan proves the point. The canary in the high debt coal mine would be loss of confidence in a country’s bonds, but since all of Japan’s bonds are purchased by Japan, it’s not a good test case. Another indicator would be a sharp decline in demand for the country’s currency. Fortunately for Japan, it’s currency enjoys a steady demand to purchase its many exported products. The Yen is also one of the “standard drawing rights” currencies as designated by the International Monetary Fund (along with the dollar, yuan, euro and pound) which gives it a special status as a chaos hedge. But, as shown in Figure 5, the Yen has experienced about a 25% devaluation relative to the dollar since the end of 2012, (although the valuation of the Yen has recovered from a low point in 2015 and the Yen has not lost value against a basket of all other world currencies). The devaluation of the Yen may be directly related to Abenomics (high debt, money creation, negative interest rates), but we don’t know to what extent.

We asked earlier what the U.S. will likely do to deal with its huge and growing debt. One possible answer lies in the Japan example. The U.S. could become more like Japan; it could let its debt grow, create money to fund the debt and sell all debt to the Federal Reserve and other government agencies. To most economists that sounds like an unattractive solution. But, another possibility exists.

Modern Monetary Theory

So far we have established that the U.S. is in deep debt, that countries that accumulate a high amount of debt relative to GDP generally face very bad economic outcomes (with the exception of Japan so far) and that QE programs have been one way the U.S. has been able to bail itself out of serious financial situations since 2008. Now let’s turn to Modern Monetary Theory (MMT)10 which has been presented as a possible solution to the current economic dilemma.

MMT is a new and different way of thinking about government budgets. The theory takes money creation and deficit spending a step beyond QE. Well, more than a step. More like a huge leap. According to MMT, government debt does not matter. That is to say the amount of government indebtedness is of no consequence. In contrast to Paul Krugman’s thinking that Debt/GDP is important, MMT proponents think the ratio is of little importance. Unlike households and businesses, as the theory goes, governments can incur an almost unlimited amount of debt because they can always create money to repay it. This idea is not only mind expanding but somewhat controversial. Almost all economists would agree that governments can incur debt and create money, but even the most other-worldly-minded would not agree that governments should create money without limit. The typical arguments made against unlimited money creation are that it can cause a loss of confidence in the currency, inflation or fear of inflation, and a rush to move dollars into hard assets or other currencies. Picture a Banana Republic outcome.

Politically speaking, the idea that “debt does not matter” has great appeal because, if true, it would solve a major source of conflict in U.S. politics i.e., how to obtain funds to meet all needs, those favored by liberals and conservatives alike. It’s easy to see how this idea would become popular amongst politicians who (not to be too cynical) need money to buy votes but don’t want to raise taxes which may cost them votes. In fact, the idea is spreading rapidly and “debt does not matter” has become a mantra amongst online devotees on Twitter and other social media platforms.

Where did this idea get started? The genesis of the idea seems to have come from a school of thought called “functional finance” originally put forth by economist Abba Lerner.11 At a very high level, functional finance is the idea that government economic policy (both monetary and fiscal) should be managed to achieve certain objectives – namely, economic welfare, full employment and price stability. Functional finance ideas were later adopted by hedge fund manager, Warren Mosler12 and several university economics professors including Stephanie Kelton of Stony Brook.13 Functional finance teaches that economic and social objectives should be obtained by government borrowing, lending and money creation. This is not such a novel idea today. It’s not unlike the way the FOMC operates. The Fed adjusts policy to come as close as possible to its inflation and unemployment targets.

The proponents of functional finance take the idea of a managed economy a step (huge leap) further. They propose that the economic policy should aim for absolute employment i.e., 0% unemployment. During lean times and when dislocations occur in the private sector, the government should step-in and employ everyone who becomes unemployed. Or, if not employ everyone, at least provide them with a guaranteed income.

So, the two ideas: “government management of the economy to achieve welfare objectives” and “debt does not matter” are a perfect marriage. They complement one another as components of a government-centric model of the economy. Envision a group of government gnomes in Washington turning economic knobs to achieve the desired results.

But MMT thinking goes beyond “debt does not matter”. The primary reason debt does not matter is because governments can create money out of the ether to repay their debt. And, it follows at least in theory that because governments can create money, they need not incur any debt at all. According to MMT logic, governments need not issue bonds nor collect taxes but need only turn on the digital printing press to pay for expenditures. Government decides what objectives it wishes to achieve, creates money to accomplish those objectives and spends the newly created money accordingly.

The founders of the MMT theory issue one caveat. They say if printing too much money causes price inflation, they’ll control inflation by imposing taxes. In the world of MMT, taxes are needed only to reduce consumption and thus, control upward pressure on prices.

To summarize, the main elements of MMT:

• Unlike households and businesses, the indebtedness of sovereign governments does not matter. This is perhaps most true of governments like the U.S. whose currency is used as a reserve currency for much of the rest of the world.

• The primary reason debt does not matter is because sovereign nations can create money to pay for expenditures just like the U.S. has done with QE.

• Because nations can create money, they need not collect taxes or issue bonds to pay for expenses, they can (at least in theory) pay for all expenditures with newly created money.

• Monetary and fiscal policy should be managed to achieve certain social objectives employing created money.

• In response to critics who say that expanding the money supply by creating new money is inflationary, the MMT proponents reply that inflation can be controlled by taxing households and businesses.

It’s easy to see how MMT could be used at least in theory to solve the current problems faced by the U.S. Newly created money could be used to repay all current creditors. Going forward either no new debt would be issued or like Japan, all debt would be purchased internally and most by the Fed. However, as in Japan, money creation on a large scale would eliminate the possibility of selling government bonds to foreign governments…because no one would buy them.

The Politics of MMT

The idea is mind boggling. Think of the political implications of MMT. Politicians could spend almost without limit. Today when politicians vote to spend money, we often hear political commentators saying things like “Is that a good use of taxpayer money?” Or, they may ask “Should we be mortgaging the future for our children?”

MMT has an answer to these kinds of objections: “Don’t worry about it.” In the utopian world of MMT, politicians need not answer to taxpayers because taxation is logically de-coupled from spending. Politicians would have no fiscal accountability to anyone. They could spend money as they pleased and answer to no one. Voters would have no reason to push back on the way the government spent money and there would be an unlimited amount of money to draw upon.

Imagine, with no concern for fiscal responsibility, the politicians who promised the greatest spending would be elected. MMT would be truly transformative. This kind of a system would surely attract huge numbers of new immigrants and with no concern for the economic effect of massive immigration, there would be no reason for any politician to oppose it. In the most extreme case the U.S. digital printing press could produce an unlimited amount of new currency to support everyone in the world, all 8 billion of us. Of course, that wouldn’t work, but the extreme case illustrates the folly of the less extreme cases.

Would adoption of such a system lead to a decline in the U.S. relative to other nations that paid their debts without creating money? Yes, it would seem so. We would see increased confidence in currencies of governments that paid their bills with taxes or sovereign debt and decreased confidence in currencies of governments that paid their bills with a digital printing press. The dollar would gradually lose its position as a favored reserve currency which would reduce demand for dollars and lead to a devaluation.

Remember, U.S. currency was once backed by gold. Anyone who wanted to exchange their dollars for gold could do so. The U.S. changed this policy in the 1970’s and since then the dollar has been backed only by the good faith and integrity of the government. MMT would take the debasement yet one step further. The dollar would be backed only by the government’s ability to create one more digital dollar without creating a panic.

The MMT proponents point to the enigma of Japan as an evidence that MMT may work. Nonetheless, it’s probably hard even for believers to imagine how long MMT would work and to what kind of endgame it would lead.

At its core, MMT is more of a political philosophy than an economic theory. It is the set of economic assumptions and policies required to give a centralized government complete control over government spending without having to answer to anyone. So, is MMT a version of utopia? I suppose only if you fully trust the politicians and monetary gnomes who would be turning the economic knobs in Washington and only if you believe it could last forever. Markets tend to experience long periods of orderly, linear behavior punctuated by infrequent discontinuities (e.g., stock market crashes, a run on banks, the COVID virus). It’s one of those discontinuities (e.g., sudden loss of confidence in the dollar) that could be the eventual undoing of MMT.

____________________________________

[1] https://www.fiscal.treasury.gov/reports-statements/treasury-bulletin/current.html

[3] https://worldpopulationreview.com/countries/countries-by-national-debt

[6] Treasury bonds are assets on the Fed’s balance sheet and equivalent new bank reserves are the offsetting liability.

[7] https://www.federalreserve.gov/aboutthefed/files/BSTFRcombinedfinstmt20072008.pdf

[8] https://www.federalreserve.gov/releases/h41/current/h41.htm#h41tab1

[10] https://www.investopedia.com/modern-monetary-theory-mmt-4588060

[11] https://en.wikipedia.org/wiki/Functional_finance