Remember when Bill Clinton was President and he placed a sign on his desk that read “it’s the economy, stupid”? He was right. It is all about the economy. Jobs, standard of living, a greater distribution of income, discretionary purchases, moving up, the American Dream, investment in new technology, foreign aid to poor countries…they all depend on the economy.

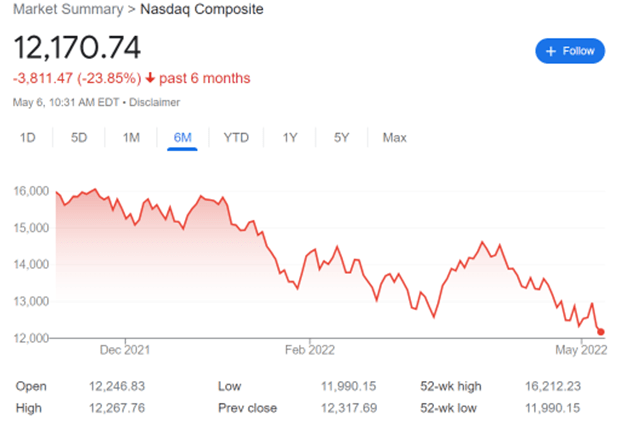

Unfortunately, today our economy appears to be headed for a recession and double-digit inflation and that is causing investors to panic and dump stocks. What’s driving this bad economy? Understanding may be helpful in devising an investment strategy.

- At the top of the list is the price of energy. Energy prices contribute to just about everything else: transportation cost, heating, air conditioning, manufacturing, product inputs. Sanctions on Russia have reduced the worldwide supply of oil and gas, but the price of oil was over $100/barrel even before Russia invaded Ukraine. Part of the blame lies with the COVID virus, if one can blame a virus. The downturn in energy demand during the pandemic caused suppliers, including OPEC, to reduce production. Then, when the economy started picking up, we found ourselves with a supply shortage. Oil companies have started drilling new wells, but it takes time before new supply comes online.

Another factor may be naive climate-change thinking: the idea that if we just make fossil fuel extremely expensive, that will accelerate the use of renewables. The idea is basically correct but making fossil fuels too expensive too fast could destroy the economy in the process, a fact that is overlooked by some zealots. It’s also not possible for consumers, businesses and governments to instantly switch to more renewables even if that were their greatest wish. The transition will take some time because of the availability and economics of the new technology and the embedded investment in existing infrastructure.

Climate change concern has also influenced government policy. Stopping construction of the new Keystone pipeline, although it may not have affected energy prices in the U.S., was of symbolic importance. It signaled that the government was going to play hardball with fossil fuels. Same with the moratorium on drilling on Federal land. It may have had no effect on the spot price or futures market today, but it sent a message to the industry.

Energy execs who testified before Congress said that clean energy sentiment in government has affected their willingness to risk new exploration. After all, exploration and drilling are expensive. Why would an oil company exec spend millions on a new well if they thought the government might place new regulations on it? At the very least, they’d be less likely to take a risk.

Energy prices are expected to come down, but only after much more supply is available. OPEC members have not been willing to increase production much. We probably need to wait for U.S. and Canadian production to ramp up, which will take a while. - Next on the list would have to be our economic policy. Two aspects of our policy are inflationary: government spending and Federal Reserve actions.

Deficit spending is inflationary and the greater the deficit, the greater the inflationary stimulus. In fiscal year 2021 the federal deficit was $2.8 trillion and in the prior fiscal year over $3 trillion. These deficits, caused by COVID and infrastructure spending programs and the downturn in tax receipts, are the highest ever.

Both parties can be blamed for the deficits. They started under Trump and continued after Biden took office. Much of the spending was to help small businesses and households during COVID, but as usual the politicians loaded lots of pork onto each of the spending bills.

We could conclude that our lawmakers have been irresponsible, but in their defense, COVID seemed to be very threatening at the time. What’s inexcusable now that COVID seems to have passed and the economy is in trouble, is to continue with more inflationary spending as some lawmakers continue to push.

The Federal Reserve, whose charter is to control inflation, has also contributed to the current mess. The Fed has kept interest rates near zero, which stimulates business borrowing but hurts fixed income investors. They’ve also maintained a balance sheet of $9 trillion. That means they’ve purchased (and not yet sold) $9 trillion in government and non-government bonds and securities. These purchases stimulate the economy and are inflationary. By comparison, the U.S. GDP is about $21 trillion and the total U.S. debt is about $22 trillion, so the Fed balance sheet is very significant (huge).

As a result of the current inflation, Chairman Powell (head of the Federal Reserve) said that the Fed will reduce its balance sheet by $3 trillion. In other words, they are going to sell $3 trillion in bonds and put that money out of circulation. That, of course, will have a highly contractionary effect on the economy. No wonder the stock market is crashing.

The Fed also plans to raise the federal fund rate by a percentage point in half point increments over the next two months. This will cause all interest rates to rise and existing bond prices to decline. So, bond holders should take note. - A distant third place is the supply chain. COVID has caused supply shortages because of reduced production (e.g., in China) and delayed delivery (e.g., cargo ships lined up at U.S. ports). Both have contributed to higher prices.

Also, Russia and Ukraine supply much of the world’s wheat and corn. This supply has been reduced by the war and sanctions against Russia.

The commodities that are now in short supply could be good investments, at least in the short run. - The feedback from a lower stock market will also be a factor. When the stock market is booming, people feel rich and tend to spend more money. When it’s crashing, households tend to hunker down and tighten the purse strings. So, in either direction, there can be a spiral effect – recession expectation leading to lower stock market leading to contracting economy and so on.

The stock market also has an effect on businesses. A dropping stock market tends to reduce the number of IPOs and also the amount of venture capital funding of start-ups. Moreover, lower stock prices and higher interest rates are the worst possible combination for financing business expansion. - Then, there’s the effect of higher wages. Somehow there’s a labor shortage in the U.S. It’s hard to understand exactly how that happened. Some say workers dropped out of the labor pool during COVID and never returned. In any event, the shortage has caused employers to raise wages hoping to attract workers. Higher wages lead to higher prices. Economists say that wages tend to be ratcheted upward, meaning they can go up but not down.

Those are the main factors that have contributed to our current economic situation. There may be other less significant contributors.

The economy affects the outlook for stocks, so understanding the factors contributing to the current economic situation may be helpful for investors.

What are investors to do in this situation? Here are a few possible basic strategies:

A. As Jim Cramer would say “sell, sell, sell”. You can sell now if you think the market will sink further. This would at least save you from further trauma. To minimize the damage, you can hope to sell on a day when the market rebounds from a relief rally. Of course, lots of people have the same idea, so that may not work.

A component of this strategy is to generate cash now and buy back when the market has reached a bottom and the economy is on the mend. The challenge is knowing when to buy back and distinguishing market head fakes from real changes in direction. This can be tricky. But, in general, selling now is not a completely irrational strategy. Obviously selling a few months ago would have been much better but that’s water under the bridge, over the dam or pick your favorite saying.

Long-term investors could also take advantage of the current depressed market to make small investments in alternative energy or other tech investments. Some may be good long-term bets at these prices and buying in some increments is better than all at once.

Of course, if the market rebounds much sooner than expected, you could end up with seller’s remorse. Everyone needs to be their own forecaster. The good news is that historically, the market tends to drop faster than it rebounds, so you may be given some early warning signs.

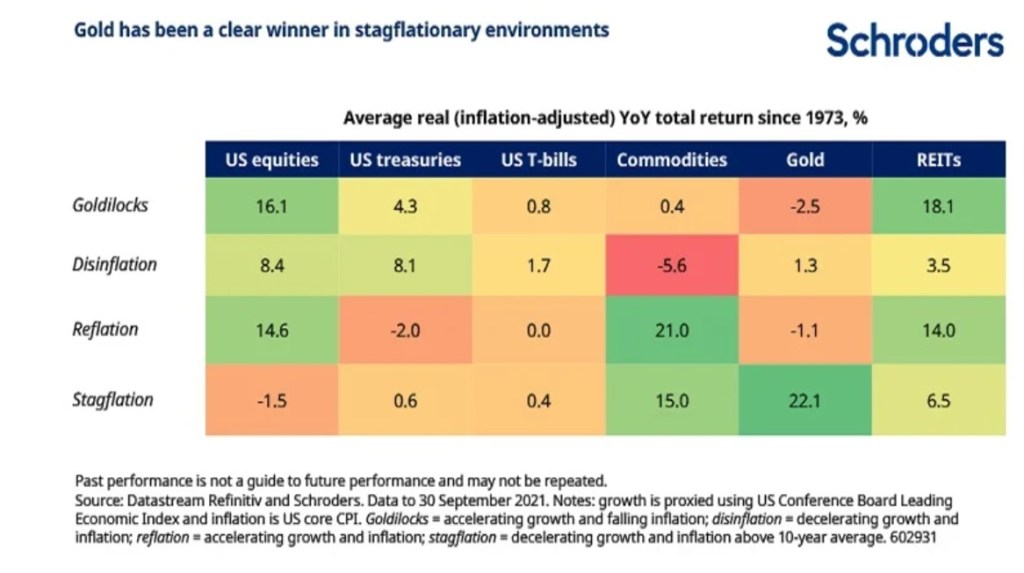

B. As every student learns in Investment 101, Diversify your investments. Normally this means spreading your money between stocks, bonds, and cash, but today bonds are paying very little and interest rates appear to be headed up, so (based on the information available today) investing in bonds seems a bad strategy. Even holding bond funds is probably not smart. Diversifying could mean selling your tech stocks and investing more in real estate, oil, natural gas, gold, dividend generators or particular stocks that will weather a stagflation environment the best. This seems like a reasonable thing to do. See chart below.

I would also want to keep some cash on the sidelines not only to invest in stocks when the market appears to turn, (see strategy A above), but also to invest in some bonds when interest rates have peaked.

C. Ride out the storm. Some of my friends have hired financial advisors to manage their money. The advisors charge .5 to 1% per year. I’m too cheap to do that and I don’t trust most advisors, but I ask my friends what their advisors are saying.

Based on the small sample size of my survey, professional financial advisors are telling their clients to stay the course.

Let’s examine the “stay the course” strategy a little. Like any investment strategy, there are pros and cons. One of the arguments against this strategy that sticks in my mind comes from my experience in year 2000. At that time, I was heavily invested in tech stocks and we all know what happened to tech stocks. I admit to being confused at the time. I thought tech stocks would recover. It was wishful thinking. I sold some, kept others and watched my portfolio tank. It took almost 10 years to recover. At age 50, while you’re still working, that ‘s not so bad although it was painful at the time. At age 70, when you’re mostly retired, it’s a riskier strategy.

On the other hand, our economists and Federal Reserve managers now have the experience of the 2000 and 2008 market collapses under their belts. Maybe they now know how to deal with this economy better. I have little confidence that this is true, but thought I would throw it out there.

Let’s also consider that we’ve just been through a 13-year bull market, the longest in history. Stock market performance following long bull markets in the past has not been good. Long bull markets are usually followed by periods of subpar performance. Of course, this information is of value only if one knows they’ve entered a bear market, a market that will perform poorly for an extended period. Otherwise, they could be experiencing a bull market correction, a market that will rebound within a quarter or two. Let’s assume for the sake of argument that we are now in a bear market. In that case, we should expect that a ‘stay the course’ strategy will lead to low equity returns for at least a few years and maybe longer.

We can also consider data showing the historical relationship between economic conditions and stock market performance. We need to do some amateur forecasting, but let’s assume we are headed to a period of stagflation. In that case, at least based on history, the best investments may be in gold and commodities. Nothing guarantees history will repeat itself, but we know that Wall Street investors at Goldman Sachs, Morgan Stanley, etc. are looking at the same data and trying to make good investment decisions for their firms or firm’s clients. So, if we are headed for stagflation or if we can assume that Goldman Sachs thinks we’re headed for stagflation, then this chart is of some value and should nudge us at least a little toward commodities (oil, gas, minerals, some foods, necessities) and precious metals.

A corollary to the Ride out the Storm approach is to generate income by trading options (puts and calls). That’s what I have been doing. Over the past two weeks it has felt like trying to extinguish a forest fire with a squirt gun, but I think it will be a helpful component of any of the above strategies.

Conclusion. Perhaps the best strategy would be some combination of A, B, and C. As your financial advisor would say “it depends on your risk tolerance” and other factors like whether you are depending on your nest egg for living expenses.

To be continued. Take with a truckload of salt and use at your own risk.